{kind=link}

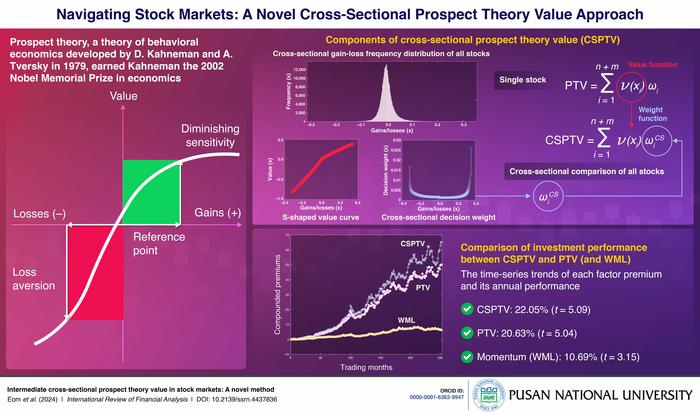

Prospect theory, proposed by Kahneman and Tversky in 1979, has been acknowledged as an excellent decision-making theory for the bounded rationality of investors tending to show cognitive bias under conditions of uncertainty. In terms of gains and losses in prospect theory, investors tend to be more sensitive to losses than equal-magnitude gains (loss aversion). Together, they show different risk attitudes: risk-averse in the case of gains and risk-seeking in the case of loss (diminishing sensitivity).

Credit: Cheoljun Eom from Pusan National University

Prospect theory, proposed by Kahneman and Tversky in 1979, has been acknowledged as an excellent decision-making theory for the bounded rationality of investors tending to show cognitive bias under conditions of uncertainty. In terms of gains and losses in prospect theory, investors tend to be more sensitive to losses than equal-magnitude gains (loss aversion). Together, they show different risk attitudes: risk-averse in the case of gains and risk-seeking in the case of loss (diminishing sensitivity).

According to a 2016 study by Baberis et al., under the premise of prospective utility, investors determine the values of prospect theory for stocks using past return distributions as a representativeness heuristic. The study defines the past 12-month return distributions as the heuristic of investor decision-making based on prospect theory.

Accordingly, a group of researchers led by Professor Cheoljun Eom from the School of Business at Pusan National University, Korea, recently empirically investigated whether prospect theory values from the past 12-month return distributions have the power to predict performance persistence for the cross-sectional returns of stocks in future holding periods. Furthermore, as the methods measuring the values of prospect theory for cross-sectional stock returns improve, they devised a new measurement of cross-sectional prospect theory value (CSPTV) to enable cross-sectional comparison among stocks, compared with the existing prospect theory value (PTV) specific to a single stock. Their study was made available online on 15 February 2024 and published in Volume 93 of the International Review of Financial Analysis on 1 May 2024.

“Our work robustly demonstrates the ability of CSPTV to outdo PTV in terms of predictive power of performance persistence,” remarks Prof. Eom.

The present study, through its research goals and results is expected to make contributions on several fronts. First, it shows the predictive power of performance persistence in future holding periods using PTVs from the past 12-month return distributions. Particularly, the scope of prospect theory for cross-sectional stock returns in stock markets has now been successfully expanded over the past 12 months. Moreover, this work devises a CSPTV reflecting investors’ tendency to compare gains and losses among stocks cross-sectionally, unlike the PTV specific to a single stock. The comparative advantage of CSPTV in better capturing the predictive power of prospect theory compared to PTV is thus empirically proven. Lastly, this study confirms that PTVs from the past 12 months can explain both the momentum and disposition effects observed during the same period. This means that the information value in a prospect theory portfolio has been robustly proven to be unique and not redundant for the above effects.

Prof. Eom concludes, “Overall, we anticipate differentiated contributions from the CSPTV design, which expands the scope of the existing prospect theory to the past 12-month return distribution and improves the predictive power of prospect theory in cross-sectional stock returns.”

***

Reference

DOI: 10.1016/j.irfa.2024.103120

About the institute

Pusan National University, located in Busan, South Korea, was founded in 1946, and is now the no. 1 national university of South Korea in research and educational competency. The multi-campus university also has other smaller campuses in Yangsan, Miryang, and Ami. The university prides itself on the principles of truth, freedom, and service, and has approximately 30,000 students, 1200 professors, and 750 faculty members. The university is composed of 14 colleges (schools) and one independent division, with 103 departments in all.

About the author

Cheoljun Eom is a professor at the School of Business at Pusan National University in South Korea. He was a postdoctoral researcher at Pohang University of Science and Technology (POSTECH) from 1999 to 2000 and worked as a manager at Hyundai Investment and Security Co. Ltd. from 2001 to 2002, where he developed the total asset allocation system. His research interests include asset pricing, portfolio optimization, financial econometrics, and econophysics. He has published many research papers in the fields of Finance and Interdisciplinary Science. After winning the 2009 Best Researcher award at Pusan National University, he has received several research excellence awards. He recently won the Korea Financial Investment Association Outstanding Paper Award at the 2023 joint conference with the Allied Korea Finance Associations for presenting an intermediate cross-sectional prospect theory value.

ORCID id: 0000-0001-6362-9947

Yunsung Eom is a professor at the School of Business at Hansung University in Seoul, South Korea. He graduated from the Department of Fine Arts and the Department of Business Administration at Seoul National University and also obtained his master’s and doctoral degrees in Finance there. He has conducted research as a visiting scholar at the University of Washington and the Economic Research Institute, Bank of Korea. His research interests include behavioral finance, market microstructure, investments, and algorithmic trading. His most cited research is “The disposition effect and investment performance in the futures market,” which is published in the Journal of Futures Markets in 2009.

Jong Won Park has been a professor of Finance at the College of Business at the University of Seoul since 2005. Before joining UOS, Professor Park was an assistant and associate professor at the College of Business at Cheju National University. He obtained his Ph.D. in Finance from Seoul National University in March 1995. His research interests focus on empirical asset pricing, market volatility, capital markets and anomalies, derivatives/risk management, retirement and public pension, corporate finance, market regulation, and macro-finance.

Journal

International Review of Financial Analysis

Method of Research

Experimental study

Subject of Research

Not applicable

Article Title

Intermediate cross-sectional prospect theory value in stock markets: A novel method

Article Publication Date

1-May-2024